Market Note

Peace dividend paid forward

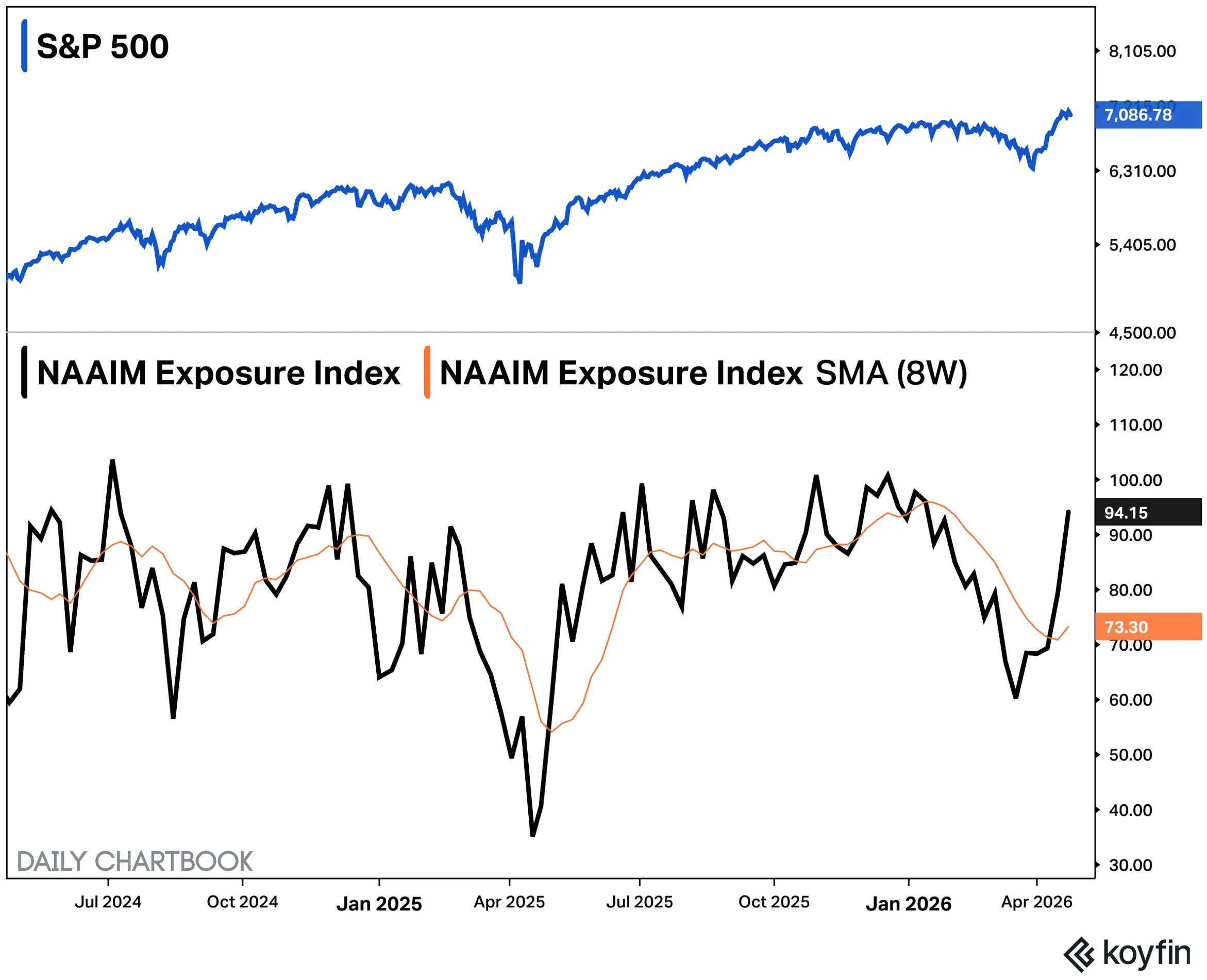

Chart Source(s): Koyfin | Daily Chartbook

The remarkable re-engagement with risk taking in the wake of the temporary cease fire has created both opportunities and challenges for hedge funds.

The initial snapback helped March HF losses recover, but there have been some dangerous short squeeze trends and headline risks remain. Although, investor reaction to Iran developments has become more subdued.

The trillion dollar question here is whether this rally is a complacent trap or recent gains are sustainable. Given the relatively muted reaction of risk assets to the shock of war in March, investors are not waiting for a resolution as FOMO envelopes investment decisions.

Global Markets & Economic Data

- Equities are consolidating after the S&P 500 made a 12.5% run off the March lows.

- US: March retail sales exploded higher driven by higher gas prices. April Michigan Consumer Sentiment registered its weakest reading on record.

- Switzerland/Europe/UK: The Swiss trade surplus hit its lowest level since February 2024 as watch exports slumped suffering from high precious metals prices and tepid Middle East demand. In the UK, March inflation was 3.3%, slightly below forecasts. The German ZEW Economic Sentiment index registered its lowest reading since December 2022.

- China/Japan: Chinese FDI fell 7.3% y/y last month. Japanese inflation is running at 1.5% annual rate.

Index Returns Summary

| Asset Class | MTD | YTD |

|---|---|---|

| MSCI World | 9.30% | 5.83% |

| MSCI Asia Pacific | 8.76% | 10.73% |

| MSCI Europe | 10.31% | 7.63% |

| MSCI China | 7.15% | -1.78% |

| Bloomberg Barclays Global Aggregate Index | 2.03% | 0.97% |

| Bloomberg Commodities Index | -2.79% | 20.60% |

| HFRX Global | 2.93% | 2.36% |

| HFRX Macro/CTA | 2.13% | 3.69% |

| HFRX Equity Hedge | 5.27% | 3.79% |

*Index data as of April 17, 2026

Market Spotlight: The case for precious metals

Precious metals prices have quietly bottomed after a tumultuous Q4 2025 through Q1 2026 run that featured a speculative frenzy which eventually popped.

During March, precious metals were treated as a risk asset rather than a diversifier due to the heavy speculative participation in the months prior.

Looking ahead, positioning is far cleaner and central bank demand remains in a secular uptrend.

Growing expectations for further fiscal irresponsibility out of G-7 politicians and increased stable coin demand are additional drivers of higher prices over the medium-term.

Chart Source(s): Financial Times | World Gold Council, IMF

Market Spotlight: US vs EU Earnings

Q1 earnings season has helped shift investor attention away from the low edge activity of geopolitical outcomes.

While the ROW ex-US equity trade remains appealing for investors, don’t count the US out just yet as the economic backdrop remains quite resilient fueled by AI cap ex.

Meanwhile, headwinds around European earnings have developed in recent months, which are exacerbated by the shock of higher energy prices.

Chart Source(s): Bloomberg Earnings Estimates Graphs | Bloomberg Opinion

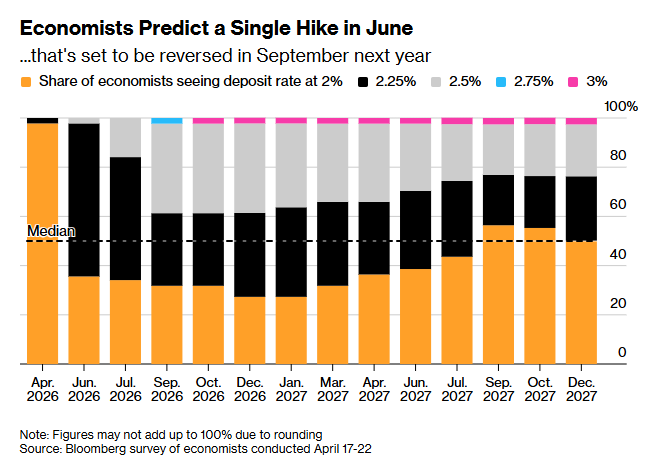

Market Spotlight: ECB could hike in June

UK inflation picked up to 3.3% y/y in March, with higher energy costs driving the acceleration.

The ECB is now expected to hike in June around the war-driven inflation.

This has led to Consumer Confidence in UK/Eurozone falling sharply from these pressures; the Ipsos Economic Optimism Index falls to record lows as 78% of Brits expect a worse economy over the next 12 months.

Chart Source(s): Bloomberg survey of economists conducted April 17-22

Have Questions or Want to Learn More?

Our team is ready to provide further insights into our strategies and the current market landscape. Reach out to us today.

Contact UsDisclaimer: This material has been prepared by MASTERPIECE ADVISORS for informational purposes only and should not be construed as financial advice. Investments in hedge funds are speculative and involve a high degree of risk. This material is confidential and may not be disclosed without the express written approval of MASTERPIECE ADVISORS.