Market Note

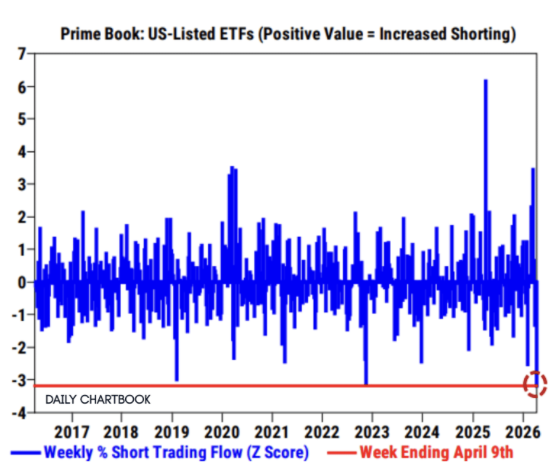

The squeeze is on!

Risk-taking appetites have swiftly rebounded following a pause in geopolitical-driven volatility.

Chart Source(s): Goldman Sachs

As hedge fund net exposures started to recede in March, equities staged a shocking recovery.

Strangely the slow bleed in equities during March witnessed an opposite pattern with the SPX “down on the stairs and up on the escalator,” as risk was clearly to the upside a few weeks ago.

The violent move higher is helping overall investor PNL, but short positions within hedge fund portfolios have been acutely painful.

Optimistically, there may be a good window to re-enter secular short stories at better price levels—if you can find the borrow.

Global Markets & Economic Data

- US: March existing home sales hit the lowest level in nine months, missing estimates. The March PPI number was below estimates at 0.5%.

- Switzerland/EU/UK: European industrial production data for February was higher than expected. German wholesale prices exploded higher in March, up 2.7% m/m, 4.1% y/y. UK February GDP grew more than expected at 0.5% m/m versus 0.1% estimate.

- China/Japan: Chinese March balance of trade numbers fell precipitously. Japanese February machinery orders were up 25% y/y.

Index Returns Summary

| Asset Class | MTD | YTD |

|---|---|---|

| MSCI World | 5.13% | 1.66% |

| MSCI Asia Pacific | 7.39% | 9.36% |

| MSCI Europe | 7.43% | 4.75% |

| MSCI China | 4.47% | -4.46% |

| Bloomberg Barclays Global Aggregate Index | 1.14% | 0.08% |

| Bloomberg Commodities Index | -2.30% | 21.09% |

| HFRX Global | 1.89% | 1.32% |

| HFRX Macro/CTA | 1.75% | 3.31% |

| HFRX Equity Hedge | 3.37% | 1.89% |

*Index data as of April 10, 2026

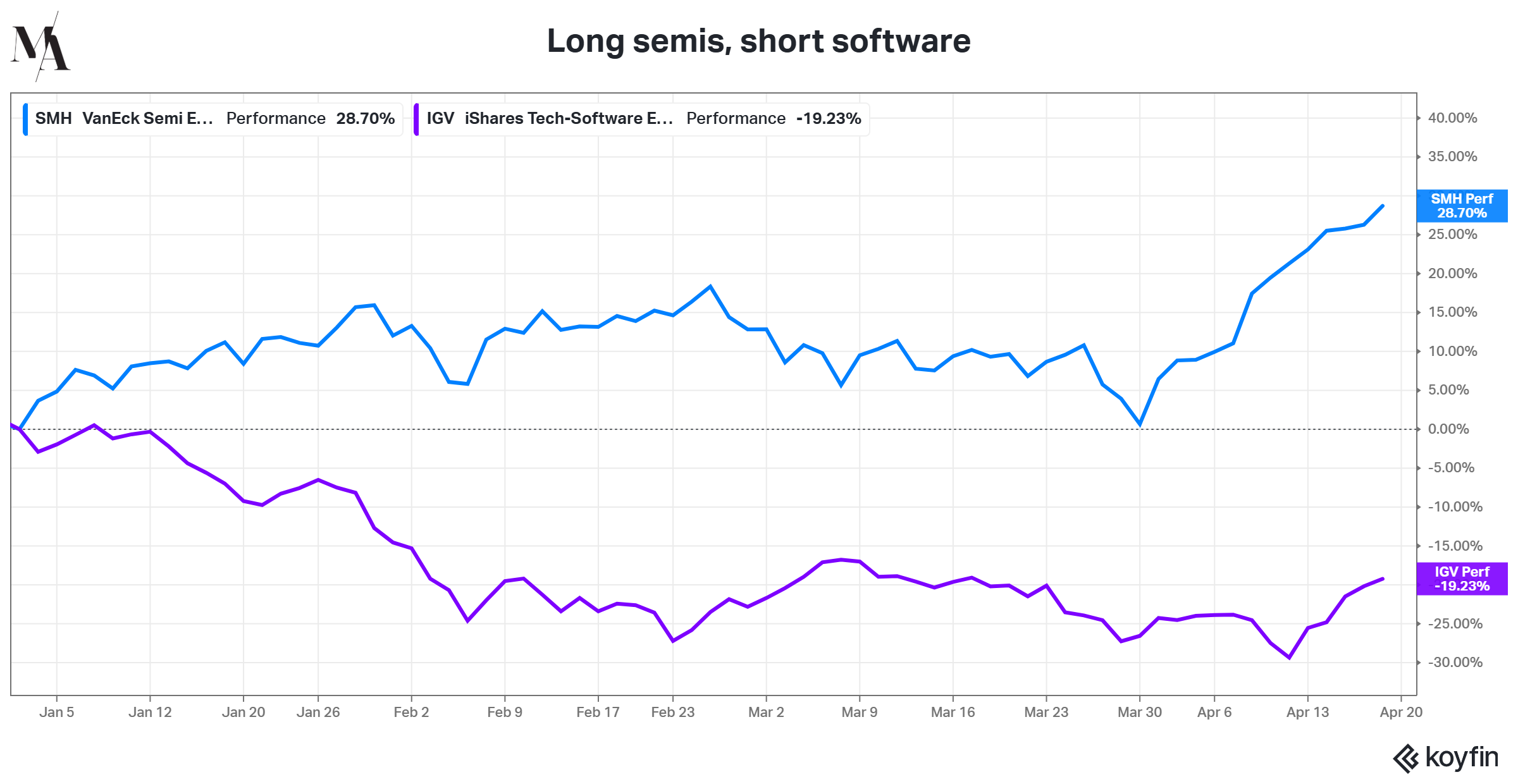

Market Spotlight: AI Trade Winners and Losers

Semis are well bid and well owned, while software is facing a secular depression.

What once was viewed as a bulletproof business model, SaaS has come into the crosshairs, mostly because there is great uncertainty on future revenue forecasts as margins are compressed amid major AI disruption.

On the flipside, chip scarcity amid red hot AI demand has caused a big need for chips and hardware.

The dispersion within the technology sub-sector underscores the vast opportunity set for technology specialist long/short funds who can identify the winners and losers.

Chart Source(s): Koyfin

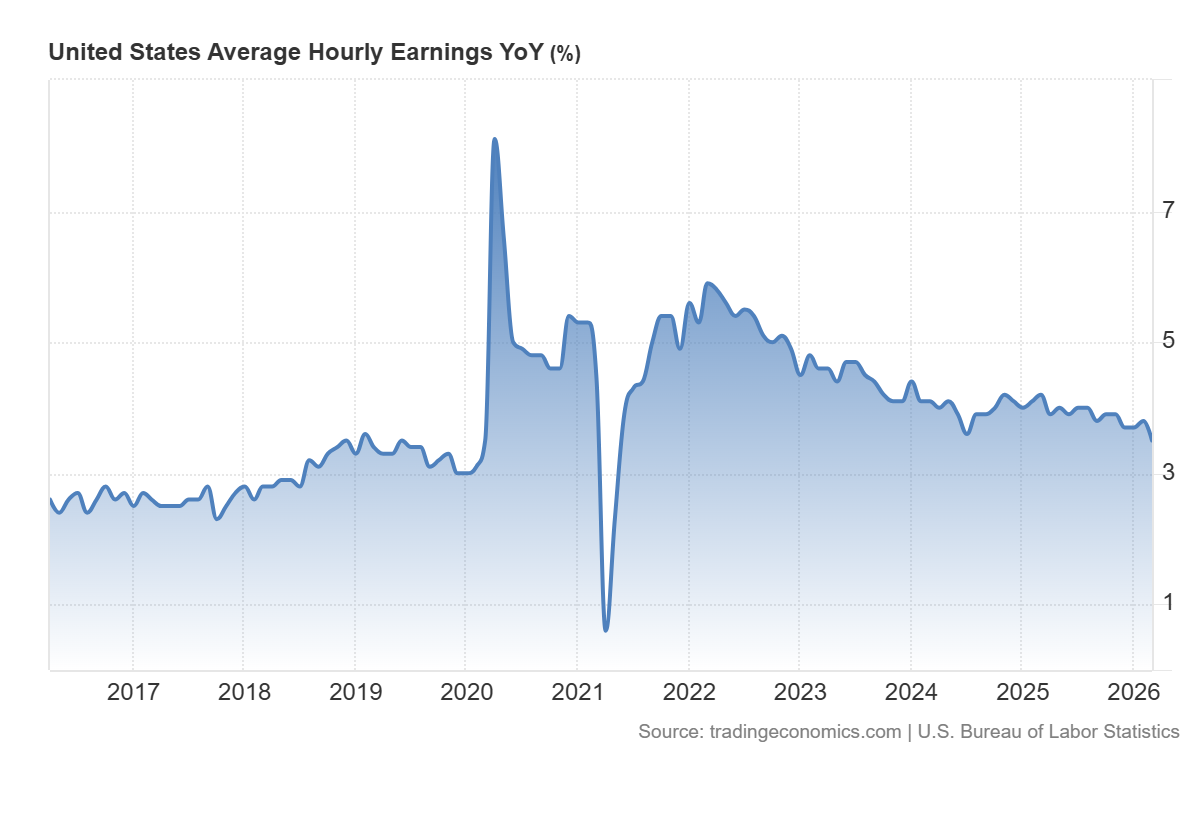

Market Spotlight: US Labor Market

The fate of the labor market is one of the most pivotal drivers of the next decade, having wide sweeping micro and macro implications across asset classes, sectors, and politics.

The US labor market remains relatively stable on a top-line basis, with the unemployment rate remaining near historical lows. Some economists have called the current state the “no-hire, no-fire economy”.

Under the surface some concerns are starting to mount around entry level job opportunities, which has kept a lid on wage price pressures, which have receded since the pandemic.

As opposed to 2022, the lack of wage price pressure currently will contribute to reduce inflationary pressures, offsetting the current energy price pressures.

Unfortunately this will continue to be an overhang on consumer spending, but thankfully animal spirits remain stoked by the wealth effect with US equities hitting all-time highs, underscoring the k-shaped two speed US economic backdrop where asset owners benefit while lower tier consumers suffer from elevated costs and constrained wage upside.

Many jobs today will clearly go the way of the ice box and horse and buggy, the hope is that the economy of tomorrow will produce enough opportunities to provide balance.

Chart Source(s): tradingeconomics.com | U.S. Bureau of Labor Statistics

Have Questions or Want to Learn More?

Our team is ready to provide further insights into our strategies and the current market landscape. Reach out to us today.

Contact UsDisclaimer: This material has been prepared by MASTERPIECE ADVISORS for informational purposes only and should not be construed as financial advice. Investments in hedge funds are speculative and involve a high degree of risk. This material is confidential and may not be disclosed without the express written approval of MASTERPIECE ADVISORS.