Market Note

No landing

February 20th, 2026

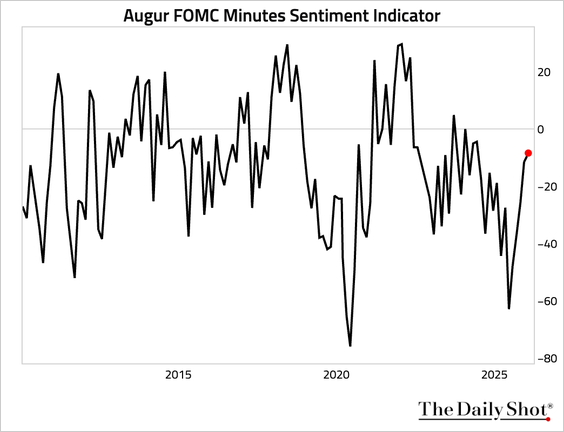

Augur FOMC Minutes Sentiment Indicator dips into negative territory

Chart Source(s): The Daily Shot

January FOMC minutes released earlier this week signaled mixed viewpoints within the Fed as some members advocate for further rate cuts while others seek to stay on hold or even raise rates if inflation data heats up.

The mixed viewpoints within the Fed are emblematic of the current market environment where investors can interpret developments from positive or negative perspectives.

Within the current backdrop secular macro trends that materialized in the past year in metals and emerging markets are working while positioning based upon micro fundamentals is providing mixed opportunities, especially in US markets.

Thin trading volumes due to US and Chinese holidays and continued hedge fund de-grossing are contributing to a directionless market backdrop.

Global Markets & Economic Data

- US: Industrial and manufacturing data points were stronger than expected and Q4 GDP is on track to hit 3.6%, which suggests far more of a mid-cycle profile than a late-cycle one. Housing starts were surprisingly positive while mortgage applications continued to weaken for a fourth straight week, but refinancing activity picked up as 30-year mortgage rates moved lower.

- Switzerland/UK/Eurozone: Swiss industrial output contracted in January while its trade surplus data strengthened from a rise in exports and a fall in imports. Expectations of further BOE easing were supported by recent soft inflation and unemployment data points with UK inflation data hitting a 10-month low and the unemployment rate hitting a 10-year high. German ZEW economic sentiment data surprisingly weakened.

- Japan/China: Japan's December Machinery Orders hit the highest level since August 2020. Chinese CNY FX trading volumes have risen rapidly over recent years to surpass CHF volumes and almost keep pace with JPY volumes.

Index Returns Summary

| Asset Class | MTD | YTD |

|---|---|---|

| MSCI World | -0.35% | 1.91% |

| MSCI Asia Pacific | 5.89% | 12.58% |

| MSCI Europe | 0.81% | 5.27% |

| MSCI China | -4.10% | 0.56% |

| Bloomberg Barclays Global Aggregate Index | 0.79% | 1.73% |

| Bloomberg Commodities Index | -2.78% | 7.34% |

| HFRX Global | -0.19% | 1.81% |

| HFRX Macro/CTA | -0.73% | 3.27% |

| HFRX Equity Hedge | -0.07% | 2.19% |

Index data as of February 13, 2026

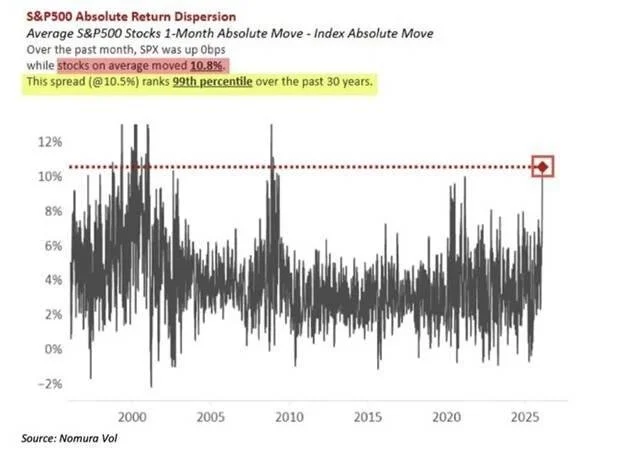

Market Spotlight: Rotations around the zero line

The S&P is essentially flat on the year while below the surface we recently registered 99th percentile movements in average individual stock movement versus the index.

Chart Source(s): Nomura Vol

Market Spotlight: ROW looks better

Get out while there is still time seems to be the mantra for global investors when it comes to considering their US allocations.

Chart Source(s): Goldman Sachs

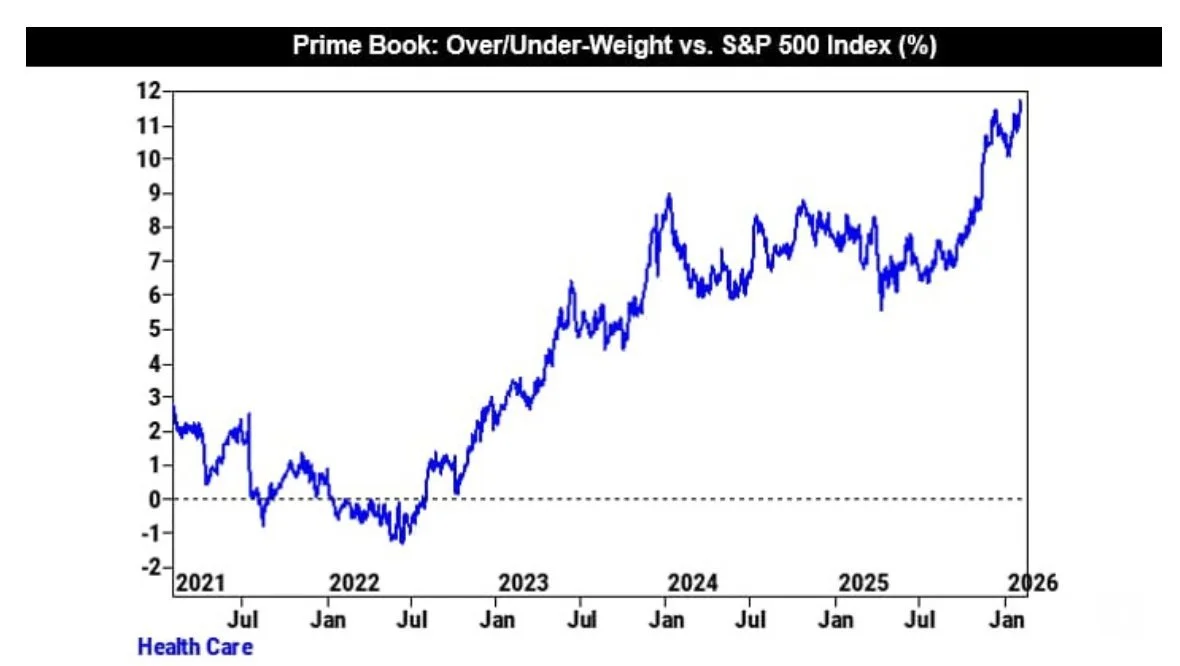

Market Spotlight: The healthcare bull case is solidifying

Hedge fund healthcare positioning has reached multi-year highs.

Chart Source(s): Goldman Sachs

Have Questions or Want to Learn More?

Our team is ready to provide further insights into our strategies and the current market landscape. Reach out to us today.

Contact UsDisclaimer: This material has been prepared by MASTERPIECE ADVISORS for informational purposes only and should not be construed as financial advice. Investments in hedge funds are speculative and involve a high degree of risk. This material is confidential and may not be disclosed without the express written approval of MASTERPIECE ADVISORS.