Market Note

Big market reversals to start 2026

A pause in the geopolitical backdrop helped risk assets to bounce with investors eagerly looking towards Q1 corporate earnings for greater fundamentally driven market catalysts.

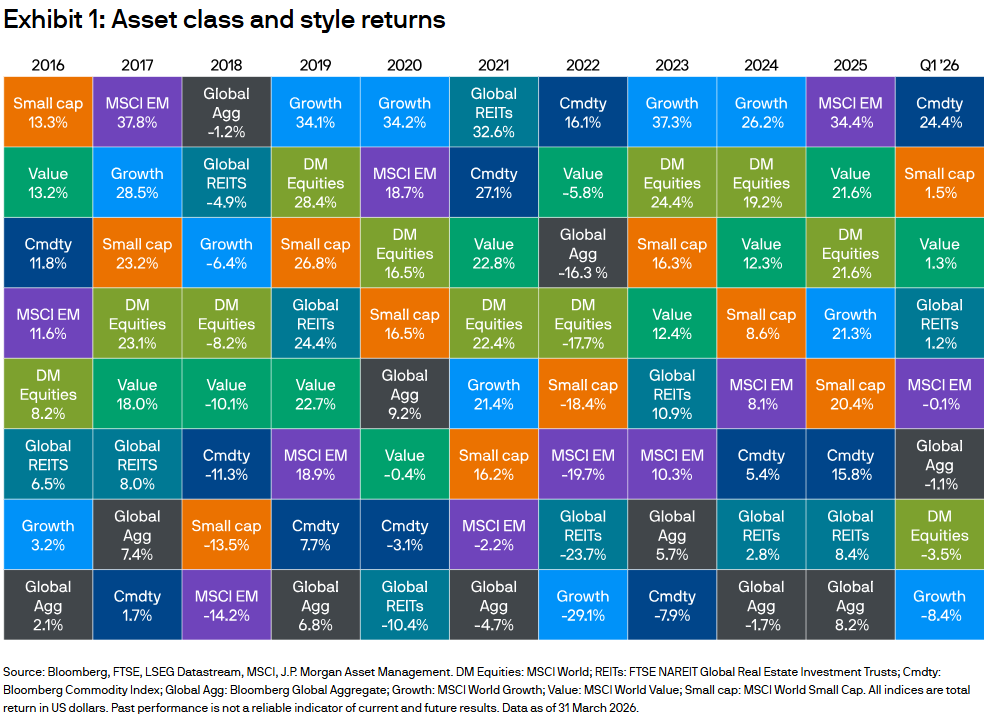

Q1 Asset Class & Style Highlights: Big Market Reversals in Q1

Commodities are outperforming YTD and on the flip-side of the Q1 leaderboard were growth stocks. In the middle we find emerging markets, who pulled ahead early in the quarter driven by a weak US dollar and growing interest among investors to diversify globally.

Chart Source(s): J.P. Morgan

Global Markets & Economic Data

- US: March ISM services PMI was 54, below 55 expectations. The annual inflation rate jumped to 3.3% in March driven by higher energy prices. Mich. Consumer Sentiment fell to a historic low in early April.

- Switzerland/UK/EU: The Swiss unemployment rate hit was 3.1% in March. UK house prices rose by less than expected y/y in March. German Factory Orders moved back into positive m/m territory in Feb.

- China/Japan: Feb. Chinese Consumer Confidence was weaker than forecast in March. Japanese Household Spending fell by 1.8% y/y.

Index Returns Summary

| Asset Class | MTD | YTD |

|---|---|---|

| MSCI World | -6.32% | -3.28% |

| MSCI Asia Pacific | -11.18% | 3.63% |

| MSCI Europe | -9.80% | -1.90% |

| MSCI China | -7.69% | -9.03% |

| Bloomberg Barclays Global Aggregate Index | -3.07% | -1.00% |

| Bloomberg Commodities Index | 11.15% | 22.16% |

| HFRX Global | -2.95% | -0.50% |

| HFRX Macro/CTA | -3.66% | 1.76% |

| HFRX Equity Hedge | -4.44% | -1.34% |

*Index data as of March 31, 2026

Market Spotlight: A look at US inflation

Headline inflation rose to 3.3% in March, its biggest increase in nearly two years, largely driven by higher energy prices while core inflation remained contained with falling used car prices, steady shelter costs, and easing food prices. Markets are pricing in more hawkish central bank outcomes due to the Iran conflict, but this appears driven more by market dynamics than economic fundamentals, creating potential opportunities in global rates, particularly at the front end of yield curves. One caveat is that food prices have the potential to move higher from here due to knock-on effects of higher energy and disruptive upcoming El Niño weather patterns.

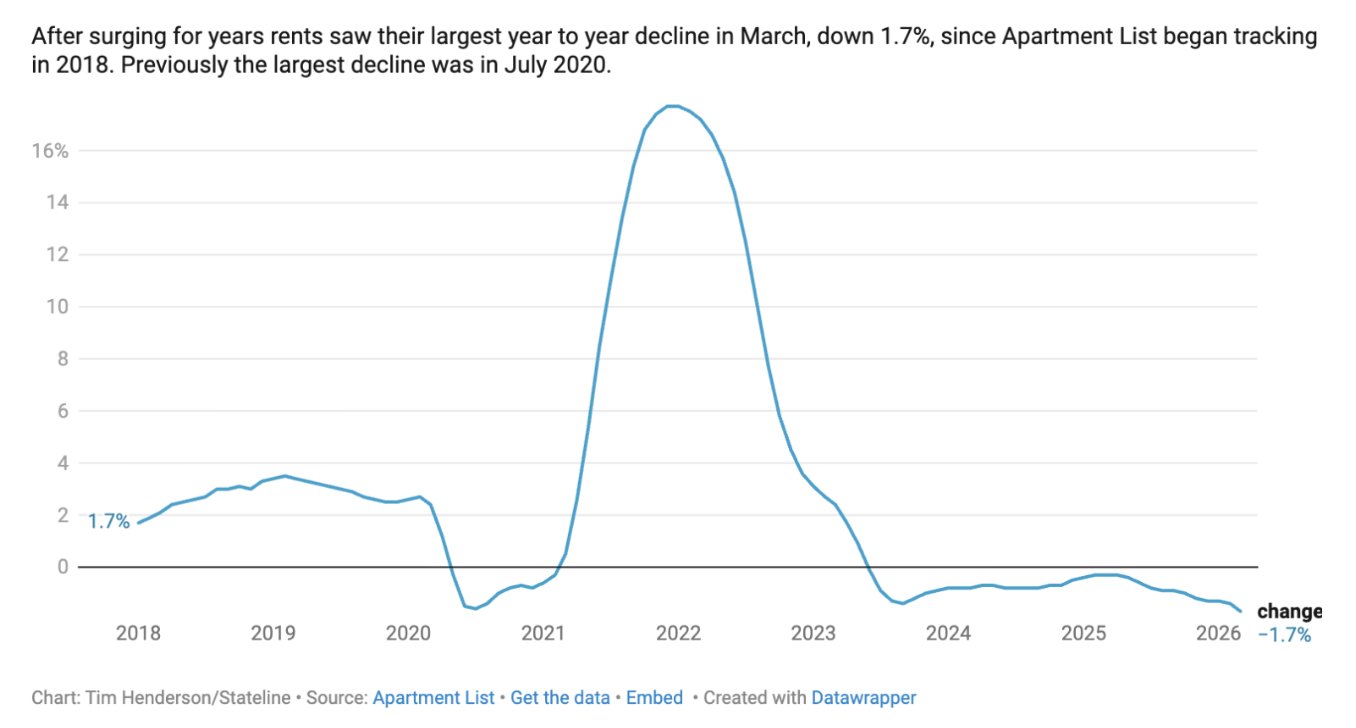

Falling US apartment rental prices

Chart Source(s): Apartment List

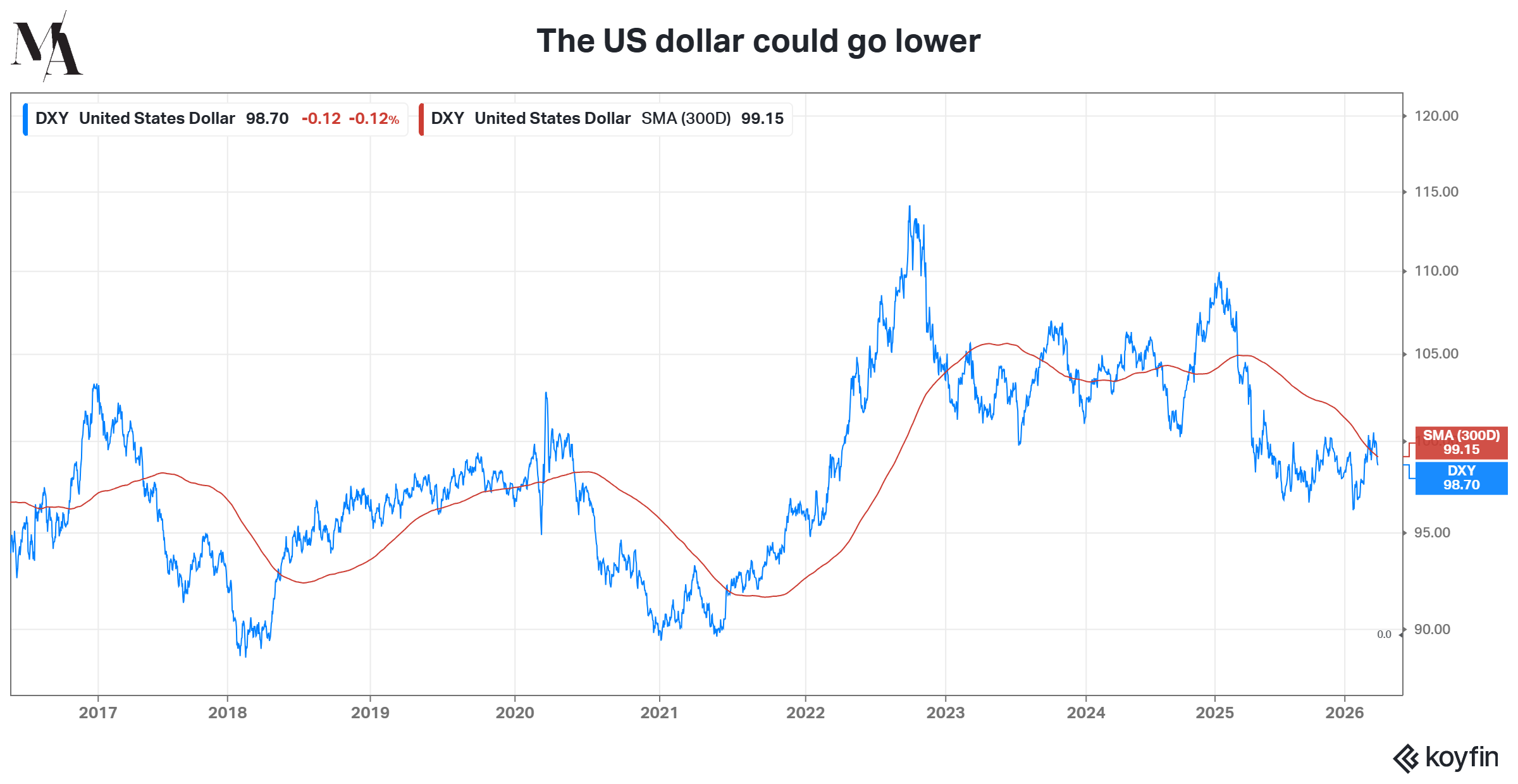

Market Spotlight: The case against the US dollar

Global Macro managers held widespread short USD positions before the Iran conflict, but the sudden dollar spike during the conflict forced painful unwinding of these bearish bets. Despite this setback, some funds maintain their long-term USD bearish stance, citing fundamental concerns including overvaluation, persistent deficits, potential rate cuts, and foreign investors potentially reducing USD exposure.

Chart Source(s): Koyfin

Have Questions or Want to Learn More?

Our team is ready to provide further insights into our strategies and the current market landscape. Reach out to us today.

Contact UsDisclaimer: This material has been prepared by MASTERPIECE ADVISORS for informational purposes only and should not be construed as financial advice. Investments in hedge funds are speculative and involve a high degree of risk. This material is confidential and may not be disclosed without the express written approval of MASTERPIECE ADVISORS.