Market Note

The risk washout

February 6th, 2026

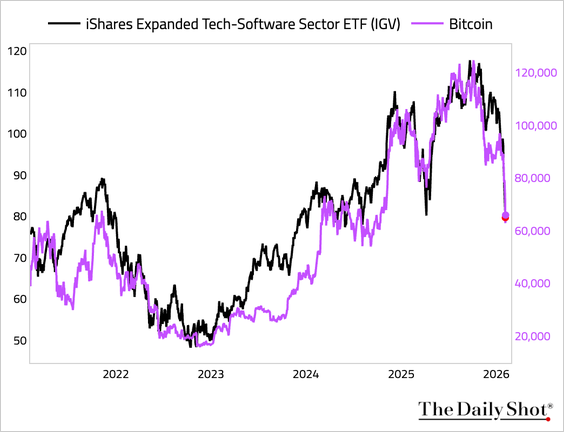

The risk washout intensifies as crypto and software sell off

Chart Source(s): The Daily Shot

As of Friday morning in the pre-market, the S&P 500 is 2% off of its "all-time-highs" reached February 2nd, but it feels a lot worse out there.

Crypto's utility function and market structure are called into question as the price plummets. Crypto treasury companies are entering dangerous territory pressuring their balance sheets, which could pressure prices even lower.

The crypto crash comes amid a loss of confidence in existing software business models due to AI replacement. The AI displacement theory in software is quite relevant but with software technicals moving into dramatic oversold territory, the sector is now rife with fundamental dislocations, probably starting with MSFT.

Multi-Strategy hedge funds are hitting performance challenges. Ongoing sector and factor market rotations, high gross exposure, high factor exposure to momentum are creating challenges for leveraged Multi-Strategy hedge fund platforms who are facing their worst existential crisis in years. Expect further de-risking price-action in markets over the coming weeks as risk management departments are called into action.

Global Markets & Economic Data

- US: JOLTS and weekly jobless numbers shocked to the downside with an increase in continuing claims and a decrease in job openings which fell to the lowest level since 2020. January ADP private payrolls numbers were positive, but below expectations and monthly NFP data is delayed until next Wed. ISM Manufacturing data surprised to the upside with the largest monthly rise in four years and ISM Services remained expansionary.

- Switzerland/UK/EU: Swiss Retail December Sales were up 2.9% y/y and 1% m/m, ahead of consensus and the January unemployment rate was a little higher than expected at 3.2%. Eurozone growth data remains on a slow uptrend with Q4 GDP hitting 0.3% and composite PMI remaining in expansionary territory. The ECB held rates at 2% and slowing inflation supports potential future easing if needed. The UK BoE held interest rates at 3.75% and house prices ticked up by 1% y/y in Jan.

- Japan: Foreign stock and bond investment flows moved higher and the BoJ increased its 2026 growth forecasts.

Index Returns Summary

| Asset Class | MTD | YTD |

|---|---|---|

| MSCI World | 1.74% | 1.74% |

| MSCI Asia Pacific | 5.15% | 5.15% |

| MSCI Europe | 4.46% | 4.46% |

| MSCI China | 4.70% | 4.70% |

| Bloomberg Barclays Global Aggregate Index | 0.94% | 0.94% |

| Bloomberg Commodities Index | 10.12% | 10.12% |

| HFRX Global | 2.00% | 2.00% |

| HFRX Macro/CTA | 4.00% | 4.00% |

| HFRX Equity Hedge | 2.26% | 2.26% |

Index data as of January 31, 2026

Market Spotlight: Rising hedge fund interest

Hedge funds are launching to the top of the list of asset classes for investors to target in 2026. Almost daily we see announcements by institutional investors of new and increased hedge fund mandates.

Chart Source(s): Bank of America

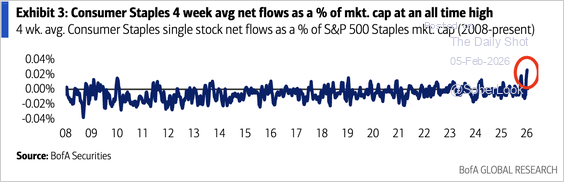

Market Spotlight: Cheap goods, soda and cigarettes

Consumer Staples names are outperforming YTD. The XLP Consumer Staples ETF is up over 12% YTD while the S&P 500 has stagnated. Top XLP ETF holdings are WMT, COST, PG, KO and PM.

Chart Source(s): The Daily Shot, Koyfin

Have Questions or Want to Learn More?

Our team is ready to provide further insights into our strategies and the current market landscape. Reach out to us today.

Contact UsDisclaimer: This material has been prepared by MASTERPIECE ADVISORS for informational purposes only and should not be construed as financial advice. Investments in hedge funds are speculative and involve a high degree of risk. This material is confidential and may not be disclosed without the express written approval of MASTERPIECE ADVISORS.