Market Note

What if AI is inflationary?

Insatiable investor risk appetite marches onwards.

Chart Source(s): The Daily Shot

Given “AI job displacement” fears have not yet been clearly reflected in the US employment numbers, one must keep an open mind about the impact of AI on the white-collar labor force of the future.

The resolution of this trend is quite impactful as labor disruptions remain one of the greatest fears of AI, cementing the secular thesis around medium term forecasts of deflation and economic slowdown ensuring an eventual slashing of interest rates back to the zero line.

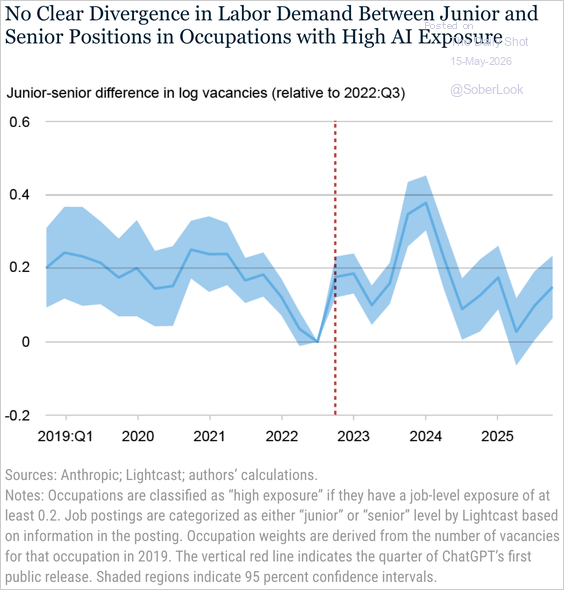

A recent Federal Reserve Bank of New York study concluded that while AI may be influencing the labor market, it is not the primary driver of the current hiring slowdown for entry-level workers.

They cite evidence demonstrating that labor demand for junior and senior roles in highly exposed occupations appears to be moving in parallel. The chart above demonstrates job postings for AI-exposed occupations show fluctuations, not a clear decline in entry-level roles after 2022. Furthermore, business surveys suggest firms are mainly planning to incorporate AI through retraining, with limited hiring effects.

Anecdotally in the financial services industry we are hearing more hedge fund business leaders mention that instead of hiring less, they are actually ramping hiring of AI savvy data analysts to further propagate their AI initiatives.

Global Markets & Economic Data

- US: Inflation data was slightly above estimates hitting a 3.8% ann. rate, while retail sales slumped. Existing Home Sales inched higher off 7-month lows.

- Switzerland/UK/EU: Swiss producer and import prices fell 2% ann. to further the country’s 3-year deflationary streak. A rise in UK political uncertainty sent government bond yields higher and its currency downwards. Germany’s ZEW economic sentiment reading rose from a 3-year low but remains negative.

- China/Japan: Chinese inflation hit 1.2% y/y in April, above consensus. Japan’s current account surplus widened, surpassing expectations.

Index Returns Summary

| Asset Class | MTD | YTD |

|---|---|---|

| MSCI World | 2.14% | 7.97% |

| MSCI Asia Pacific | 2.69% | 12.88% |

| MSCI Europe | 0.74% | 5.13% |

| MSCI China | 3.25% | -2.36% |

| Bloomberg Barclays Global Aggregate Index | 0.56% | 0.73% |

| Bloomberg Commodities Index | -1.50% | 26.69% |

| HFRX Global | 1.00% | 3.39% |

| HFRX Macro/CTA | 1.16% | 5.59% |

| HFRX Equity Hedge | 1.72% | 5.59% |

*Index data as of May 8, 2026

Disclaimer: This material has been prepared by MASTERPIECE ADVISORS for informational purposes only and should not be construed as financial advice. Investments in hedge funds are speculative and involve a high degree of risk. This material is confidential and may not be disclosed without the express written approval of MASTERPIECE ADVISORS.